Organic Products Without Intermediaries.

Second andalusian Plan of organic

farming 2007-2013.

CONTENT

DIAGNOSIS OF THE STATE SECTOR 2002-2006

Agricultural production

Economic accounts of organic farming in 2005

Livestock production

Economic accounts of organic livestock in 2005

Industrial Production

Auxiliary output

Certification

Aid and investment

Advice and training

Research and technology transfer

Marketing

Promotion of organic production and consumption

Environmental and socioeconomic effects in rural areas

COMPLIANCE PLAN FOR ORGANIC FARMING ANDALUZ 2002-2006

Goal 1. Support for organic production

Goal 2. Organizing and improving the availability of specific means

of production for agriculture and livestock ecological

Goal 3. Improve the level of knowledge of organic production systems

Goal 4. Preparation and processing of organic products

Goal 5. Structuring the field of organic farming

Goal 6. Adapt the systems of certification and control

Objectives 7 and 8. Promote awareness and disseminate information on

organic foods. Promote consumption of organic products

Goal 9. Enhance training in the sector of organic farming

Goal 10. Boosting R & D & T in the specific sector of the AE

42

Programs developed under SAAP 43

II OBJECTIVES OF THE ANDALISIAN PLAN OF ORGANIC

FARMING 2007-2013

Axes and objectives of the Plan

AXLES, GOALS AND MEASURES

Axis 1: Support of organic production

Axis 2: Support the handling and processing of organic products

Axis 3: To develop the domestic consumption of organic food

Axis 4: Enhance the training, research and technology transfer

Axis 5: Ensuring Transparency and protection of organic production

Axis 6: Promoting women's participation in the organic sector

Axis 7: strategic sectoral and territorial planning

Investments under the II Plan Andaluz de Agricultura Ecológica

DESCRIPTION OF MEASURES

Measure 1. Encourage the development of agricultural

production and ecological farming

1.1. Maintain and update the aid to promote organic farming

1.2. Maintain and update the aid to promote organic livestock

1.3. Maintain and update the aid to promote the organic beekeeping

1.4. Promoting the use of organic varieties at risk of genetic erosion

1.5. Encourage the use of organic livestock breeds in danger of extinction

1.6. Support the establishment of young farmers

1.7. Support for the modernization and improvement of organic farming

1.8. Cooperation for development of new products, processes and technologies

in the agriculture and food sector

Measure 2.a. Improving the knowledge of organic

products and their economic and environmental efficiencies.

2.1. Preparation and publication of technical materials to the operators.

71

2.2. Development of environmental and economic accounts of the Organic

Farming

2.3. Studying the contribution of organic farming to climate change

mitigation

2.4. Strengthening of the consortia for the development of organic products

2.5. Collaboration with local public entities for the development of

knowledge of the productions

ecological

Measure 2.b. Develop an advisory system, organic producers

2.6. Provision of advisory services to meet the conditionality

2.7. Provision of specialist advice in the CAP

2.8. Provision of expert advice to groups of organic producers

2.9. Creating a knowledge management system which allows access to all

available information related to organic production

Measure 3. Developing the means of production

plant

3.1. Supply of organic matter for fertilization of ecological systems

3.2. Creation and maintenance of the center of biodiversity of Loja

3.3. Supporting actions for conservation and utilization of local plant

genetic resources

3.4. Promote the control of pests and diseases in organic farming

3.5. Promote the development of specific machinery for the needs of

organic production

Step 4. Developing the means of production animal

4.1. Supporting the production deficit for 85 organic livestock

Step 5. Develop agri-ecological

5.1. Promote the processing and handling of organic products

5.2. Promote quality food in the organic industry

5.3. Study of the regulation and production of the organic industry

craft

5.4. Improving the production of organic oil

Step 6. Developing the domestic market for organic

food

6.1. Supporting companies with organic farmers to plan production, and

market concentration of supply in the domestic market

6.2. Clustering for the concentration of supply

6.3. Support the development of social and institutional consumption

of organic food

Step 7. Public benefit and environmental health

of organic foods and promote their use in any field of action

7.1. Institutional promotion campaigns

7.2. Support the organization of events and other activities designed

to promote consumption of organic food products

7.3. Support the organization of BioCórdoba

7.4. Supporting publications sector

7.5. Support for social organizations and local entities engaged in

activities relating to the development of production and consumption

of organic food

7.6. Supporting the dissemination of the benefits of organic farming

through the channel 98 HORECA

Step 8. Enhance training in the sector of organic

production

8.1. Development of dissemination of knowledge of agriculture, livestock

industry and eco -

8.2. Impetus to the creation and development of a graduate program in

Andalusia on organic farming

8.3. Designing specific training actions for the uptake and conversion

to organic production sector

8.4. Increasing the supply of organic content of the training programs

in the food industry

8.5. Conducting training for technicians in production

Step 9. Boosting R & D & T in the specific

sector of organic production

9.1. Maintenance and expansion of research in ecological agriculture

through the implementation of projects in public R & D in connection

with the priorities of the sector

9.2. Attention to the private and public demands in the field of R +

D + T in agroecological systems

9.3. Integrating the activities of technology transfer, training and

experimentation in the field of organic production

9.4. Encourage collaboration with other research for organic production

Measure 10. Improving systems of control and transparency

of the certification of agriculture, livestock, industry and environmental

inputs

10.1. Develop standards and skills for improving the control system

of organic farming in Andalusia

10.2. Developing the system of inspection and monitoring of the CAP

operators

and organic certification and coordination with other governments involved

in the process

10.3. Establish an official register of organic operators Andalusia

10.4. Develop specific rules adapted to the Andalusian

10.5. Establish mechanisms to reduce certification costs

10.6. Develop cooperation with the general consumer retail outlets in

the inspection

Measure 11. The coexistence of organic production

systems with other

11.1. Promote the protection of crops against environmental pollution

11.2. Promote regulatory and administrative instruments to prevent contamination

of organic production by genetically modified organisms

Measure 12. Promoting quality program

12.1. Producer participation in quality programs

Step 13. Develop a strategic plan of production

and gender

13.1. Supporting the development of a strategic plan of production and

gender

Measure 14. Encourage women's participation in

the organic sector

14.1. Promoting initiatives of women in the organic sector

14.2. Enhancing women's participation in the organic sector

14.3. Encourage collaboration with other governments on gender issues,

organic production

Measure 15. Develop strategic plans horizontal

sectoral and territorial

15.1. Develop sectoral strategic action to boost production

15.2. Development of organic farming in protected natural areas

15.3. Development of organic production in areas of special interest

SYSTEM OF MONITORING AND EVALUATION OF THE II

ANDALUSIAN PLAN OF ORGANIC FARMING 2007-2013

In the period ending (2002-2006) there have been two events of great importance for the sector of organic farming in Andalusia: the first has been the development of the Plan Andaluz de Agricultura Ecológica (SAAP), which defined priorities sector, established lines of action and gave them a budget to develop the second has been the creation in May 2004 of the General Directorate of Ecological Agriculture (DGAE) within the Agriculture and Fisheries, which has possible to develop from a single center of SAAP management tasks, executing the budget, expand and initiate new lines of action not contemplated originally in the SAAP.

The development of the Plan Andaluz de Agricultura Ecológica

2007-2013 allows the update of the objectives of the plan earlier in

the context of organic production and consumption in Andalusia.

The situation of the industry has changed a lot since the conditions

under which started in 2002 to the present. The actions that were raised

then have been developed especially since the creation of DGAE. Moreover,

this agency is taking actions that were not originally included in the

previous plan to suit the changing needs of the industry.

If you plan in the past emphasized the support at the production's challenges

through a consolidation. To a large extent, this translates into the

boost to domestic consumption and channel marketing, product diversification,

development of agro-industry and defending the interests of one sector

with an already significant presence in Andalusia

Below is a key dynamic in the sector, which, while not exhaustive, provides the background necessary for the drafting of the Plan Andaluz de Agricultura Ecológica for the next seven (2007-2013). Something to discuss in detail the production sector, is briefly the evolution of different land use (agriculture, livestock and processing) as well as other areas of great importance for the production of Andalusia.

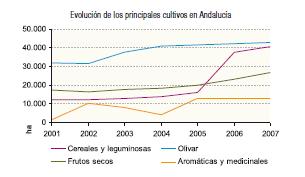

Agricultural production

The area devoted to organic production as traders have grown at a pace

much higher than the rest of the Spanish territory, putting Andalusia

as Community Leader of the production, with 60%

the surface and the Spanish eco-third of the operators. The area classified

as organic or in conversion has grown considerably since 2001, when

it had 107,000 ha, up to June 2007, 584,550 ha. In parallel, the number

of producers has increased by over 50% to reach 6855. While before 2001

the area of forest and gathering wild was responsible at a high rate

of growth of the AE, in this period the largest growth in production

is due to increase in the area of pasture and fodder (for livestock

), which grew at an annual rate of 48%. The farm grew steadily until

2007 at a rate of 27% per annum, with particularly important areas of

the cultivated olive trees, almond trees and cereals. Citrus doubled

its small size during this time, and vegetables, an important sector

for the growth of the domestic market, its size increased at a rate

of 19% per annum.

It should be noted that the largest areas of forest, pasture and fodder

are located in western Andalusia, while the east is more specialized

in Andalusian agricultural use.

Within the organic agricultural sector, the olive crop is the largest

(42,987 ha) and continues to grow, currently standing just under 3%

of the olive in Andalucía. Factors may have influenced this growth

are the ease of conversion to organic may present to the olive, the

campaigns of mass trapping (biological control of olive fly), the amount

of aid to production and improvements in technical management of the

olive grove. As current and future constraints include a certain difficulty

in the management of soil, fertilizer and deficient use of low ground

cover, and lack of oil in certain areas. Olive production is therefore

in a more advanced stage of development than other areas but still can

not transform imbalances and market the oil volume potentially available

organic. This has been the case in the province of Huelva, where there

has been no ecological mill until 2006.

The next largest use is the area of cereals and legumes, which occupies

40,000 ha. The area devoted to cereals has increased continuously until

2005, experiencing strong growth in 2006, which doubles its size, especially

in the province of Granada. This growth can be good news for the livestock

sector, which has been experiencing difficulties accessing certain feed.

However,

Study on materials for pienso3 that there are significant imbalances

in the structure of production, mainly wheat and there is a shortfall

in grain legume seed. This structure of production not only reflects

a deficit in the production of legumes for feed and human consumption,

but also indicates a deficiency in the crop rotation of crops (cereals

and pulses alternating between mostly), so important for nutrition and

stability organic farming.

Within the prevailing nuts almonds, with over 95% of the surface of this category. The area planted to almond grows steadily (7%) since 2002 and has a total of 26,618 ha, of which 88% is located in the provinces of Almeria and Granada. This exploitation is difficult to market their produce under organic certification, so the reasons for the increase would have to look into a grant obtained by the production and ease of conversion. However, it should be emphasized that the obstacle course, have disappeared aid to improvement in quality and marketing of nuts, which did not permit the maintenance of a vegetation cover. This problem has been of prime importance when considering the level of erosion that this practice entails. This situation is extensible to chestnut in some areas of Andalusia, as the valley of Genal in Malaga. It must be mentioned the potential of chestnut in Andalusia. Still, this cultivation Find deep crisis, such as putting the area of greatest production, within the Natural Park Sierra de Aracena and Picos de Aroche. Of 4700 has chestnut, in 2003 some 1,600 were certified organic. In 2006 1.350 remain certified. In studies conducted in 2004 highlighted the difficulties in marketing of organic chestnut, although their easy entry into ecológico4 crop. This situation appears to have resulted in a sharp decline in the ecological area.

The area devoted to aromatic and medicinal plants is already the fourth largest in area. Production is concentrated in the provinces of Almeria and Granada are to highlight the significant fluctuations in that area has been suffering from this use. Is to evaluate the economic importance of this sector that relatively little is known.

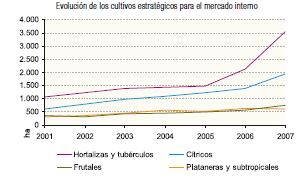

The area sown to vegetables has grown at an annual rate of 19% from

2001 to 2007, although during the years 2003 and 2004 the growth was

much lower. In 2006 there were 2136 has horticultural and tubers, that

have passed ha in 3573 to 2007. It is important to address the low organic

horticultural area in the provinces of Jaen and Cordoba, in comparison

with Almería province a leader in this aspect. You can also add

that the area devoted to protected crops (glasshouse) has fallen slightly

(8%) in the past two years, continued in 2006 with 165 ha, which accounted

for 8% of the organic horticulture.

One factor that characterizes the organic vegetable production is an

important part that is oriented towards exports, taking advantage of

well established channels and demand from other countries, mostly Europeans.

Furthermore, this production is concentrated in very few products, mainly

tomatoes and cucumber.

Moreover, diversified vegetable production is poorly developed, if this

strategy is the most efficient way of supplying the domestic market

could provide the stability and autonomy and commercial farmers. A diversified

vegetable production is also of great importance to the ecological stability

of the farming system, improving fertility and health prevention of

crops. You must search for suitable commercial channels to redirect

this and balance the market balance between external and internal, which

could allow more choice to farmers.

We have to take into consideration the smallness of the amount of aid

for organic gardening, which represent a very small percentage of farm

incomes.

Citrus and subtropical fruit crops are of great strategic importance but are very poorly developed. Citrus and subtropical share very export-oriented, especially the latter, which dominates the avocado. Organic fruit production is very low, especially when served for consumption on the domestic market potential, judging from data on consumption of fruit in the ecological and consumer associations in the conventional market. This is a strategic sector to raise a development of the domestic market, although the logistical difficulties of fruit (mainly conservation) hinder the implementation of small-scale initiatives.

And especially citrus fruits, have significant difficulties in production, associated with the management of pests and diseases can say in general that there are deficiencies in the technical knowledge available in Andalusia.

To end with the agricultural uses, no vine to wine raises serious technical difficulties in dry, so it shows a strong potential for conversion. The limited development that presents (812 ha) can be attributed in part to the weak linkages to the transformation because most of the wineries turn green only its own production.

The case of the certified forest area and wild collection is unique

because it experienced a large increase in 2002, going from 23,000 to

almost 134,000 ha, and have since increased slowly until 2007 was 162,000.

Economic accounts of organic farming

in 2005

Final agricultural production (crop and livestock) has been estimated at € 141.7 million in 20055. This result takes on greater significance if compared with its conventional equivalent area. Thus, the estimate of the Final conventional agricultural production amounts to € 88.8 million, a 35% lower than the estimated amount that the PFA Ecological € 123.1 million.

Organic farming in Andalusia in 2005 generated a Final Agricultural

Production (ATP) estimated at 123.1 M € horticultural being 34.3%

the most important economic sector, followed by olive, citrus and subtropical

30.8%, 12.2% and 7.6% respectively. In total, these four crops account

for 84.9% of the PFA and add nuts (6.2%), these five groups represent

91.1% of crops, the rest being distributed between

fruits (2.7%), crops (2.3%), aromatics (2.2%) and grapes and wine (1.7%).

We should add that when comparing these results to groups with equivalent

conventional crops, horticultural crops out so relevant. The calculation

considers a 72% increase in Production Final Ecological Horticulture

that Convencional. For citrus fruit is of particular interest, since

the PFA is an Ecological 200% higher.

Green also stresses the vines, reaching 100% above the conventional.

In contrast, crops, nuts and olive AFP obtained a very similar to the

conventional.

So far there has been a lack of end market of organic products. 14%

of the PFA from conventional sales. Of € 104,016,865 in sales and

generated organic product, 64% came from exports. The estimates are

handled on the proportion of sales of products such as conventional

or exports have proved to be far greater than the data actually point

to. Although there are products such as horticultural and citrus with

a large proportion of production to exports (73% and 86% of the organic

market, respectively), changes it is experiencing market in Andalusia

Green points to a gradual increase in sales in the domestic market in

coming years.

Wage employment in farming result of adding permanent employment, casual

and family paid an estimated eventual UTAs in 2500 with a total compensation

of 26.1 million. Unpaid employment rises

1792 at Utah, with a total of 4292 UTA.

Final production of olives (including oil) in 2005 was estimated at

€ 37,949,385, corresponding to 31% of the PFA. Remember that the

area under olives in 2005 totaled 44% of the agricultural land (this

proportion has fallen to 33% in 2007). Paid employment was 1,204 UTA,

48% of the organic sector, with the biggest difference. The unpaid also

is the largest sector, with 955 UTA.

It has been estimated at 66% of oil production (in kg) which is grinding

the organic farmers themselves, the rest is sold as conventional for

other mills for grinding. The proportion of self is less than 0.5%.

The organic oil is intended to 30% for export.

Vegetable production is the most important economic sector, contributing € 42,227,729, 34% of the total, despite occupying only 1.6% of the area in 2005 (in 2007 this proportion had increased to 2.7 %). Horticultural products generated UTA 697. Production under plastic, representing 36.2% of the horticultural PFAE and 16.4% of the total PFAE, occupying 22% of the horticultural area and 0.2% of the total ecological. Almost all of the horticultural production is sold as organic, estimated exports at 73%.

As for fruit production, has distinguished citrus and other subtropical fruit trees. The production of citrus amounted to € 14,987,423, the subtropical € 9,404,490 and the remaining fruit to € 3,288,492. Together account for 22.5% of the total PFA. Occupation generated by this sector amounted to 416 DAP. Of the 209 UTA generated citrus, 34% of them paid. This ratio is reversed in the case of sub-105 to the ALU that generates 78% of the workforce is paid. In other orchards, permanent employment, casual and family eventually paid is estimated at 51%.

Over 90% of production is marketed as organic (92% citrus fruit, 99%

of the rest). However, sales in the country are 14% in the case of citrus,

33% and 60% the sub the rest of fruit.

Livestock production

The ranches are concentrated in the mountains northwest of the region and south of Cadiz, areas where the 80% of organic farms in our region. This area is also where it concentrates much of the conventional livestock Andalusia.

It is interesting to begin by highlighting the dramatic increase in

the area of grassland (the growth rate between 2001 and 2007 is 48%,

with a surface current 287,134 ha), which has made clear to the Andalusia

head to the rest of Spain. Andalusia is the first producer of organic

livestock in Spain, with a predominance of cattle farming, which in

2005 accounts for 48% of the farms in Spain and sheep meat, accounting

for 54%. In Andalusia, the majority of farms are beef (51% of total),

followed by sheep (32%).

This increased area pastable may be related to agri-environment, taking advantage of the large proportion of the territory that ranching can be certified easily.

The beef cattle is growing at a rate exceeding 43% annually since 2001,

reaching 703 explotacionesny 50,800 heads in 2007. This growth has occurred

in the western provinces, while most of the production of grain is found

in the provinces of Granada and Almeria. For now, this rapid growth

has not been balanced with the development of infrastructure for marketing

of meat or feed supply. You can point to greener pastures aid to explain

some causes of the growth of cattle farming, which in certain areas

are closely related to large areas in detail.

The meat sheep farms are located mainly in Huelva, Seville and Cordova.

The problems faced by this sector have much to do with the previous

case, noting in any case, the easier logistics, which is related to

a reduced need for priming.

The goat meat is a much smaller area than the previous ones, with commercial characteristics similar to sheep, although the market is less enthusiasm for this kind of meat. Be taken into account that the sector remains stable in the number of organic farms as a whole, despite significant fluctuations within each province, so it can deduct a certain instability in the sector.

It must be said that this type of cattle is not very demanding in the

quality of feed and other products and that a large proportion of food

resources for priming can produce their own livestock. Nor will require

substantial investments for the priming of the animals, as the rules

required to be performed outdoors, while allowing the end of fattening

some confinement.

With regard to the stages of initiation, sacrifice and sharing in general,

momentum dissociates to the farmer of these actions in most cases. Since

this situation puts the farmer at a disadvantage, organic livestock

should consider not to follow the conventional model and involved beyond

the simple production. Thus, much of the marketing channels can be made

in full (especially the great selling restaurants, retail chains and

even some butchers) which necessarily requires no cutting.

Pig farms certified as organic have reached a peak in 2004 with 64 holdings,

dropping the last three years to 36. Most of them are in the mountains

of Huelva. Some of the reasons why the certification does not seem to

have found acceptance among farmers are the price that has been set

for conventional pork, qualities associated with pork adehesados ibérico

systems, the higher production cost of pig ecological and poor marketing

of organic meat in general.

However, the positive experience of small industries related to their

own sausages ranchers are getting a foothold in the market and finding

a good reception to their products.

The poultry sector is not in the same situation as other products. Poultry

farms have not increased since 2001 to the extent that others have done,

having also reduced the average size markedly.

Farms devoted to egg production has declined over the past three years, after reaching a maximum of 17 in 2004, while beef farms have 5 versus 2 they started in 2001.

Among the technical problems that limit the development of poultry production

may be cited difficulty in poultry and the scarcity and price of organic

feed with high protein content, such as soybeans, but also the shortage

of slaughterhouses specialized in slaughtering chickens. These factors,

along with a possible inefficient process are identifying high production

costs, especially for meat. This situation affects an important market

development, given the low price of chicken. The situation of low growth

in the poultry sector, such as the pig is similar to that in the rest

of Europe.

Organic milk production has a number of goat farms of medium size, widely

dispersed by geography Andalusia. There are a small production of cheese,

but no production of liquid milk. The production of milk and dairy products

in Andalusia has a great potential due to the presence of cattle, such

as the county of Los Pedroches and existence of indigenous breeds of

dairy goats with great skill, as the Murciano-Grenadine, Malagueña

and the Payoyo, in both cases with access to natural pastures. At present

is considering support for specific projects in this regard, allowing

the introduction of the milk market in the Andalusian environment.

Beekeeping has been experiencing a steady increase overall, but like

the case of goats, with important territorial imbalances so far. Growths

have been taking place at provincial level in the following year had

become worse. The problems faced by the sector come from different sources.

From the point of view, there are difficulties in the conversion time

after the application of an allopathic product synthesis. Because at

this point, the Varroa remains a serious problem, with only one commercial

product available in Spain for ecological use (thymol). From the point

of view, organic honey sharing the problems of low domestic consumption

than the rest of the livestock sector.

Given the spectacular growth of the grass surface, the imbalances between livestock production and marketing difficulties, we can say that the organic livestock sector is very unstructured. As noted above, a major cause can be found in the access of agri-environment.

In the area of livestock and in light of some of these problems can

be of great interest to refer to strategies that some farmers are developing.

Reducing the use of feed offset by increased grazing is allowing some

farmers to the Sierra de Baza (Granada) to improve the profitability

of their livestock, reducing slightly the production. Also beginning

to be organizational efforts and involvement in the marketing opportunities

associated with the quality of organic meat. These activities are examples

to support and know they are working on solving some problematic aspects

of the industry.

Finally, you can refer to aquaculture, animal production and eco-mode

which is novel. The rearing of trout and green sturgeon, which takes

place in an Andalusian company Riofrío for over ten years, is

a pioneer in Spain and has opened the door to other producers, serving

as a basis for discussion of a specific level national, currently in

development. In addition, it is to acknowledge the work done by the

Association CAAE in developing a standard for organic aquaculture production.

Furthermore, the ability to differentiate the products of marine aquaculture

in stamp production has attracted the attention of producers Andalusians,

who proposed the creation of a standard to support its certification

activity for species of brackish waters. The General Directorate of

Ecological Agriculture is planning the imminent publication of a specific

rule to regulate marine aquaculture and is expected to benefit from

the same group of traders, producers of seabass and seabream.

Economic accounts of organic livestock in 2005

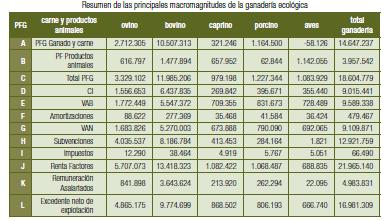

Organic livestock in Andalusia in 2005 generated an estimated final production at 18.6 million euros of which 78.8% (14.6 million) relate to the final production of Meat and Livestock and 22.2% (3 2 million) to the final production of animal products.

Paid employment, either permanent employment, casual and family wage

is estimated at 505 DAP. Unpaid family work is estimated at UTA 255,

which coupled with gainful employment shows a total occupancy of 760

UTA.

The beef sector generates 64% of the total PFA (€ 11,985,206).

Of this, 10.2% is generated from the sale of manure. The employment

generated by this sector amounted to 352 DAP, with 91.5% paid.

It should be noted that organic milk production stood at € 1,313,770,

of which 46% correspond to 35% goat and a sheep.

The pig livestock contributes 6.6% of the PFG, € 1,227,344, of

which 5% for sales of manure. This generated 171 UTA livestock, 88%

and paid the highest proportion among employment generated and PFG.

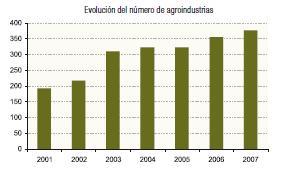

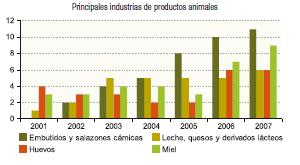

Industrial Production

The industrial sector encompasses a wide range of activities from handling and processing of food and other organic products. The number of industries in Andalusia is quite significant compared to other communities in Spain, reaching 377 in 2007, a figure second only to that of Catalonia.

The mills are scattered throughout the provinces of Andalusia, unless a clear deficit in the province of Huelva, where there is only one. Also, do not seem to be growing at the same rate they could make the surface olive green. In fact, although this time there are about 60 mills, they do not meet the demands of the potential conversion of the olive sector.

We assume that part of this problem can be overcome in the process of

being given the support in the handling, processing and marketing in

the mills accounted for 24% of companies benefit from the 2005 call

and 18% in 2006. These grants can help to create lines of milling organic

new and existing facilities.

The handling of horticultural products has increased

considerably since 2001 levels, which had 43 industries. This sector

has been the other big beneficiary of the support to the transformation

mentioned above, with

36% of the benefiting companies in 2005, with 74 facilities in 2007.

The concentration in the areas of Almeria, Granada and Malaga demonstrated

the relationship of many of these companies with the main production

areas and export orientation. Much of these companies have no direct

link with agricultural production, while controlling its supply to a

large extent, so there may be a strong producer of vegetable, citrus

and subtropical to these companies. Despite this, we can say that companies

run their production to export have no trouble finding outlets at this

time.

The wine industry also fails even to seize the opportunities of production

would be expected from the available, although the number of wineries

is now 18. Stocks were generally correspond to the transformation of

production undertaken by the farmer. These products are well received

in the market, unlike most industries certified, have a tendency to

process only organic product.

The evolution of other industries (and other canned vegetables) has

been slow from the 50 that existed in 2001 to 84 in 2007, compared with

other industries. The main limitation is the difficulty expresada6 marketing

and most of which are directed towards a diverse, including national,

where it is difficult to compete with the price of conventional products.

One feature that seems to share these with the oil industry is

the combination of organic and conventional products, so as to diversify

its supply.

For the marketing of their products, questions to consider may be the

first treatment by these industries as organic delicatessen, as a product

of high quality, high price, and furthermore the lack of receptivity

domestic market towards green products made with some difference in

price with respect to conventional. There are the sharp rise in prices

experienced between 2001 and 2003 conventional canned vegetables (+73%),

which was not so pronounced in the case of ecological (+33% in ecotiendas,

+44% in supermarkets) resulting in a reduction of the price difference

between organic and conventional canning (in 2003, this difference was

between 130% and 160%, the data correspond to the city of Cordova) 7.

It is interesting to recall what has been stated earlier on feed mills:

there is an insufficient number of feed mills between livestock sector,

but is currently being done to solve this problem and in fact, the number

handlers of grain has increased from 5 to 2 that existed in 2005.

Processing industries livestock products make up only 15% of the total

industry and many of these processors transform their own production.

Although a small proportion of the industry and also the departure of

commercial livestock production, or because it is not too difficult

to find on the internal market. You can point out that these industries

are linked mainly to the pig and dairy products, specifically those

with fewer processors. It follows that there is a large deficit in the

marketing of beef and sheep, which do not have the necessary organization

for commercialization of production available.

Empowerment in slaughterhouses slaughtering lines for organic livestock has grown significantly. At the end of 2006 there were 17 certified slaughterhouses located in all provinces of Andalusia.

One of the main problems is the industry lies in the health measures

required by law and that due to the investments required, is limiting

further development of the processing of products, particularly small

industries related to production.

Auxiliary output

This section examines the state of the means of production that farmers use, which are mainly plant material, fertilizer and plant protection, feed, machinery and veterinary medicines. Seedlings and seeds are of great importance due to the recent EU requirement to possess organic certification. Moreover, the problems of fertilizers and plant response to a paucity of information on the distinction between those that are used in ecological systems and those who do not. On the other hand, took up the issue of feed for livestock, as well as medicines.

With regard to plant material, the situation has changed slightly for

2001. There are still gaps in the collection of seeds and seedling nursery.

While there are some companies that provide seedlings for vegetables

(10 nurseries), it is noteworthy absence in western Andalusia. The supply

of certified seed is still very low in terms of diversity and still

does not take into account the traditional varieties. The legislation

does not provide, or the sale or exchange between farmers. In the study

by the Red Andaluza de Semillas thereon to DGAE detailing the status

of this problem, which relates the compulsory use of organic material

to the limited supply available in seed (for lack of diversity) and

seedlings by some logistical deficiencies.

Taking into account the proportion of farmers using own seed, 34% of

cereals and legumes and 43% of vegetables, which added 4% and 15% respectively

using certified organic seeds, you get that there is still a significant

amount Farmers unable to buy organic seed, which requires permits to

be justified mainly on the use of varieties not included in the base

of datos8. We must also produce a greater tendency to seed itself in

those of family farms and individual versus collective or corporate

farms. This reflects a strategy of greater autonomy in the family or

individual.

With regard to the nurseries, none is devoted solely to organic production

and in fact no more than an average 5% of its activity, but nurseries

declared the intention to increase this proportion.

The use of traditional varieties is offsetting much of the shortage

of diversity in crops, as there is a high degree of knowledge and use

by the farmers. This contrasts with the lack in growing woody. Organic

production is the best production system for the use of these varieties,

for mutual benefit which provides: adapted varieties are more efficient

in an ecological system and serves as an organic production system in

situ.

It is necessary to create a favorable legal framework for recovery and

maintenance by the farmers of plant varieties and traditional livestock

breeds, which are generated by the rural communities around the world,

are a collective good. Incorporation into organic production will largely

depend on institutional support for recovery and maintenance, the effect

of legislation limiting or preventing access to this resource, the productive

use of these varieties and, finally, playback and sharing of seeds among

farmers.

But there is a greater risk to the genetic heritage of Andalusia and

in general for organic products and for the maintenance of traditional

systems in general. Without any control the proliferation of commercial

crops of genetically modified organisms (GMOs), without legislation

to prevent their arrival in the ecological food chain, can cause severe

damage to organic farmers (and indeed has resulted for example in Aragon).

The release field seeds for commercial purposes may result in Andalusia

genetic contamination of organic crops, many of them made with traditional

local varieties, causing a double effect: first, the exponential multiplication

of GMOs in the food chain and the field (with effects on biodiversity),

and secondly, the economic impact on organic producers, who are deprived

of their right to produce and offer GMO-free foods, having to carry

their organic production to conventional market. The coexistence of

both production systems, organic and GM in the current conditions it

is quite difficult. To further this lack of regulation, an uncertain

future looming for the survival of organic crops that are genetically

modified counterpart, unless you begin to develop initiatives committed

to the protection of these systems.

In the field of fertilizers and the like, the main problem regarding

the use of these inputs is in the ambiguity of Regulation 2092/91 (which

is not sufficient to define the criteria for the use of inputs) and

the absence of mandatory certification to contribute to clarify this

situation, to this point is the dispersion of powers between central

government and autonomous, and this situation is particularly acute

in a context of high use of external inputs in agricultural systems,

it is also the economic difficulty of getting local manure or other

organic waste. In this sense, DGAE is implementing actions to ensure

adequate supply of organic fertilizer for organic farming. Among the

materials for the collection of organic fertilizers include manure from

the cattle and sheep, as sources of organic matter and animal waste

from the mills as a source of organic vegetable organic matter. Working

in the line activities to promote composting and creating a network

that facilitates the connection between supply and demand for compost.

Regarding the plant, most of the products listed in Annex II B of Regulation

2092/91 are only available in some European countries. The requirements

for registration of pesticides often insurmountable obstacles for these

products, be less effective than conventional or by having a lower market

to justify the costs of opening the file. A major point of discussion

copper fungicides are: producers fear that would restrict the use of

copper fungicides before becoming efficient alternatives available.

Another point of discussion are the inert ingredients in commercial

products. Many agencies and institutions believe that this may complicate

the regulation of organic products. However, at this moment there are

no criteria for generalized inert.

In addition to efforts to move forward administratively into the regulatory aspects of inputs and provide information regarding the products used, would be of interest to meet the challenge of reducing the external dependence of farms regarding these ancillary industries.

One factor limiting the development of organic livestock feed is the

availability of adequate, with insufficient numbers of certified factories

to produce and equally insufficient production. As for animals, the

most demanding in the processing of animal feed and its quality are

the bird up as the production of meat. Also the feed for finished lambs

requires a high quality and processing, like that of the calves. The

remaining guidelines are not needed for the ground and feed grains supplied

no such difficulty in supply.

Despite the calls for aid for the processing of organic products for

the payment of subsidies to cooperatives for the establishment of production

lines of organic feed, has not been received

any requests made in the two calls. Given this reality, DGAE commissioned

a survey to locate the most appropriate support depending on the needs

of industry and the effectiveness of inversión10. We identified

two entities are appropriate for this action: one in the west of Andalusia,

with the largest number of farms and the other in the East, with more

producers of grain. The procedure chosen is the creation of two joint

ventures (49% contribution of funds by the Ministry) to carry out the

expansion of production capacity, with gradual withdrawal of public

capital. It is expected that in both cases the beginning of a new activity

begins in the second half of 2007.

The study was carried out in this regard also directs its recommendations

to improve trade relations between grain and livestock producers. Areas

to be considered for these actions correspond to the increased presence

of cattle: the north of Cordoba, Seville and Huelva and Cadiz in the

countryside.

Respect to veterinary drugs include the lack of expertise on the possibility

of using alternative and homeopathic medicines for livestock, as well

as that at the moment is developing new legislation in this regard.

Finally, we should note the lack of a specific machine, according to

the concept of appropriate technology, sustainable agricultural production

requires. You need a machine that can satisfy the needs of current practices

in organic production, in particular those covered management, soil,

grass, etc.. In addition, we must take into account energy efficiency,

so as to improve the energy efficiency of existing work and contribute

to reducing emissions of greenhouse gases.

Certification

The 2002-2006 plan described in paragraph certifying how evolved the

control system in Andalusia until the situation in 2002, with three

private certification authorities. Since then and Decree 268/2003 establishes

the

registration of inspection bodies and certification, including organic

farming.

Until then, it was the Directorate General for Industry and Food Quality

who had acted as the competent authority for organic farming. When the

decree 204/2004 establishing the structure

organization of the Ministry of Agriculture and Fisheries, the powers

are as follows: Directorate of Industries and Food Quality is responsible

for the registration of inspection bodies and certification, it is appropriate

that the approval of certification, provided that there is a report

favor of the Directorate General of Organic Agriculture, which holds

the balance of skills on organic farming in Andalusia. Agri-environment

for organic farming are managed from the Directorate General of the

Andalusian Fund of Agricultural Guarantee (FAGA).

With the advent of the new structure of the Ministry and recording of inspection and certification bodies, and with Decree 166/2003 on organic production management, it undertakes the inspection bodies and certification to be accredited with respect to UNE-EN-45011. Secondly, to authorizing the same is required of an audit by the PAC, led by the advice of the DGIC DGAE. In 2005, the DGAE, using its powers and mandate of the R (EEC) 2092/91, performs oversight of all supervisory bodies, releasing a report that goes to the European Commission. Therefore, the control agencies receive three audits: ENAC, DGIC And DGAE.

Since the DGAE are making a great effort on certification, and several

areas in which work is:

• Harmonization of the operation of the certification system through:

a) meetings of the Committee for the Certification of the Andalusian

organic production which meets 2-3 times a year, b) within the Commission

there is a working group of inputs that works in this direction, c)

monitoring the above in this respect, d) communications procedure that

agencies should undertake to control DGAE, e) Establishment of period

for withdrawal of certification of operators.

• Launch of a verification protocol of the control system through

field visits by technical traders organic.

• Processing of the complaints to the operators of organic production.

Given the situation of some deregulation of the sector is expected to

increase the requirements in the compliance certification.

• Management of Retroactive Recognition of the conversion period.

• experiments are underway for the introduction of participatory

guarantee systems (GPS), which can provide a solution to reduce certification

costs for smallholders, strengthening producer groups.

Aid and investment

Organic production is subsidized to the surface in terms of lost profits and increased costs associated with organic conversion. These grants are part of the agri-2 in the axis of the EAFRD and the number of applications has grown steadily since it began in 1995. For the 2004 campaign, the average support for agricultural area in Andalusia was € 2699 per farm, € 13,189 in the case of livestock and the bee 5328 €. It is important to note that in the case of aid for ecological farm, 77% of beneficiaries have been olivar holdings. You can also mention the case of aid for organic livestock and how 59% of requests granted, which is less than 100 ha farm, receiving only 34% of the total. Ultimately, this situation stems from a poor aid regulation which led to the national legislation in force during the previous frame and their limited adaptation to the needs of the sector and its internal structure.

In that sense, have identified deficiencies in the amount of some use.

It is especially the case of horticultural crops, both outdoors and

in protected cultivation. Producers feel totally inadequate amounts

awarded, taking into account the difficulties of handling organic crops

and the significant proportion of their costs. According to available

studies for cherry tomatoes and asparagus grown in protected outdoor,

aid accounts for 1.5% and 1.4% respectively of the Value Added Neto11

12. You can see that this amount is totally irrelevant.

The DGAE has been supporting the development of the sector from different

fields to contribute their structure. Especially noteworthy has been

the annual call for support in the handling, processing and marketing

of products from organic farming. These grants have had a very positive

reception in the area of agribusiness. However, it still make a greater

effort to promote the use of such aids with Finnish society and business.

Thus, in the call for 2005, grants for a total of 26 projects, out of

79 admitted. Of these, 9 were handling horticultural projects, 7 mills,

2 vegetable, 8 other activities. It should be noted that only one project

is devoted to Finnish society and marketing. The total amount granted

in 2005 amounted to € 1,373,915.

In the 2006 call has been received 109 applications, twenty-three more

than in the convocation of 2005, of which 45 cases have been resolved

favorably (19 more than last year), with a total of 2,891,820.63 euros,

assuming an increase of 1,517,905.63 euros to the call of 2005 (increase

of 110.5%).

As for structuring the sector is also actively promoting the association

to support changes in society, within a step towards greater sustainability,

eco-friendly agricultural production and healthy eating. In this sense,

was convened in 2006 an order for grants to nonprofit organizations

and local authorities for actions to promote and develop ecological

agriculture and livestock.

Other grants that have been promoted from DGAE match the grant for the

control of the olive fly, support for attending trade fairs, support

for social consumption, and so on. Of note is the intention of leading

the great majority of the amounts directly to operators.

Advice and training

One of the actions foreseen in the previous plan was to set up in the Agriculture and Fisheries, an advisory service for organic farmers. Previously there were only trained professionals and the advice was mainly either by the technical personnel of enterprises, or by certified personnel. This advice is not the responsibility of certification authorities.

Since the DGAE has created an advisory service in collaboration with

a network of technicians organic producer groups. In 2005, three technicians

were recruited from DGAE, so that the function of centralized counseling.

That same year, a call for groups, cooperatives and producer associations,

as well as agencies and farming organizations. Through a network work,

begins to be a system of operational advice. In 2005 he hired regional

field technicians 5 to 10 who joined in 2006: 1 in the provinces of

Cordoba and Malaga, 2 in Almeria, Cadiz,

Granada and Huelva and 5 in the Seville. In this context, it is very

important to develop an advisory system that supports the organization

of producers, allowing technical assistance, as well as the continuous

recycling of

personal counseling through the coordination of the proposed service

DGAE. The current advisory service will have to modify its structure

to adapt to the demands of the new European framework, which is expressed

through the Rural Development Program 2007-2013 Andalusia.

The powers vested in the training of producers currently on the Research

and Training Institute for Agriculture and Fisheries (IFAPA), so that

coordination between administrations as a key element must conform to

deliver environmental management techniques to producers. It is worth

mentioning the limited supply of specific courses on organic farming

and the absence of a specific training program in organic farming.

Are taking other training initiatives, by certification authorities

and farming organizations. Here we must highlight the important work

that the Association has played in CAAE training of farmers and professionals.

The Consortium for Research and Training Center on Ecological Agriculture

and Rural Development of Granada (CIFAED) also has numerous training

activities. The lines that have been working have been training

in production techniques with farmers and ranchers, as well as organic

food and responsible consumption and its relation to health.

Regarding the training of technical staff, is being introduced in a

formal training college for the content of organic farming. The training

facilities available are limited to optional subjects, in

best, in some universities of Andalusia; specialization courses in organic

farming in two Andalusian universities (Universidad Internacional de

Andalucía and the University of Seville), and offered a master-doctorate

from the International University of Andalusia and of Cordova, mainly

students from Latin America. Despite being an offer exceeding that of

other communities in Spain, the improvement of formal training for technicians

is a basic pillar for the future development of the sector.

Regarding content, the problems highlighted by the agricultural sector

is apparent and a little training in environmental management in general,

with special attention to the use of fertilizer and organic matter management

techniques adventitious and those aimed at the prevention of pests and

diseases. The problems of organic farmers who are mostly influence on

feeding and animal health. Taking into account the difficulties expressed

by the agribusiness sector, would be of interest to include training

on the special requirements of agro-ecological training modules accordingly.

Finally, we have identified deficiencies in many companies in the sector

on trade and marketing.

At present, the technical knowledge available largely in Andalusia meets

the above demands, except cases.

As a challenge, it may be desirable to take into account the interest

of creating systems for training and advice on organic production, additional

measures to assess the current, such as updating the staff on these

issues in the Agriculture and Fisheries or the largest use of farm partners.